For MCA funders and brokers, business loan files rarely arrive clean. Submissions come from emails, portals, and partners, often with bank statements, identity documents, and other official documents mixed together.

Under high volume, manual intake makes it harder to spot document fraud, such as altered documents, fake bank statements, or mismatched details.

That’s how document fraud slips into everyday loan processing and creates unnecessary risk.

A clear workflow changes this, and that means clean structure, early organization, and consistent file prep help teams review submitted documents with more confidence.

In this article, we break down how document fraud shows up in business funding and how to manage it without adding extra review steps.

TL;DR

- Document fraud in business funding often hides inside everyday loan files like bank statements, utility bills, and registration documents.

- Common fraud patterns include altered documents, reused templates, real documents used for the wrong business, and inconsistent details across files.

- Manual workflows make fraud harder to catch because files arrive out of order, reviewers rely on visual checks, and legacy systems fragment the review process.

- Teams reduce risk by following clear best practices: standardized intake, consistent document grouping, early consistency checks, and clean handoffs to credit teams.

- Heron supports document fraud review by scrubbing and organizing submissions before review, surfacing missing data and inconsistencies early, and preparing review-ready business loan files without replacing human judgment.

What Document Fraud Means in Business Funding

Document fraud refers to using false documents or misleading information in a business loan file.

In business funding, this usually shows up in bank statements, utility bills, or registration records that do not fully match the business applying for funding.

Unlike consumer funding, commercial files often mix many legitimate documents with small changes.

Some files include altered documents, forged documents, or even entirely fake documents that look close to genuine ones. Others rely on real paperwork used in the wrong business context.

This makes document fraud harder to spot in business funding. Reviews often come down to comparing documents side by side, checking consistency across files, and noticing small gaps during the verification process.

When files arrive unstructured, manual review slows down and increases the risk of significant financial losses.

In business funding, document fraud often blends real and fake information inside one digital file rather than appearing as obvious fraud.

Where Document Fraud Shows Up in Business Loan Files

Document fraud in business funding usually hides inside everyday paperwork, not obviously fake files. Funding teams often see issues in documents they review every day.

Common problem areas include:

- Bank statements and other financial statement files with small changes, mismatched totals, or signs of document alteration

- Proofs of address, such as utility bills, that include falsified details or reused information

- Business registration documents that do not match public records or show unusual formatting

- Reused or mismatched files that appear across multiple submissions, sometimes linked to fraudulent templates

In many cases, files mix authentic documents with altered sections. Others rely on image files edited with basic software or scanned after physical edits, a form of pre-digital document modification.

Because these submissions often include real data alongside changes, you depend on structure and careful review to support document verification and detect fraudulent documents during the normal review process for businesses applying for loans.

Why Business Loan Files Are Structurally More Exposed to Document Fraud

Business loan files carry more built-in complexity than most other funding contexts. That complexity creates more room for document fraud to hide, even before review begins.

Unlike single-form submissions, business loan files are assembled over time. Bank statements, applications, proofs, and supporting records often arrive in stages rather than all at once. This makes it harder to see the full picture early.

Multiple parties also touch the same file. Brokers, ISOs, merchants, and internal teams may all submit documents at different points. Each handoff adds variation in format, naming, and completeness.

There is rarely one source of truth document in business funding. Files depend heavily on PDFs, scans, screenshots, and emailed attachments rather than structured forms.

On top of that, business loan submissions vary widely by industry, deal size, and funding type. What looks normal for one file may be unusual for another.

Common Document Fraud Patterns Teams See

Document fraud in business funding often follows a few repeat patterns. These issues usually arise during routine reviews, not as overt fraud attempts.

Below are the most common patterns MCA funders and brokers encounter in business loan submissions:

Altered or Edited Documents

You can often see document alteration where genuine documents include small changes. Numbers, dates, or names may be adjusted using basic editing software or image files.

Some cases involve pre-digital document modification, where physical edits are scanned back into a digital file, making issues harder to spot during review.

Template-Based Documents Reused Across Deals

Some submissions rely on fraudulent templates reused across multiple business loan files. These files may look consistent on the surface, but they repeat the same layout, structure, or formatting across different applicants.

This pattern often points to document mills supplying falsified documents at scale.

Real Documents Used in the Wrong Business Context

Not all fraud attempts involve fake paperwork. You can sometimes receive authentic documents used for the wrong business, address, or entity.

This can overlap with identity theft or synthetic identity fraud, where real and fake information appear together in one file.

Inconsistent Business Details Across Files

Inconsistencies across bank statements, registration records, and other documents are common. Legitimate data may appear in one file but conflict with other documents in the same submission.

These gaps make it harder to detect fraudulent documents without a clear structure and careful review.

Why Document Fraud Slips Through in Manual Workflows

Manual workflows make fraud document detection harder as business loan volume grows.

Submissions arrive from many sources, and files rarely follow the same order or format. Teams spend time sorting documents before they can even start reviewing.

Under time pressure, repeated manual checks rely heavily on visual inspection and human oversight. Small signs of document manipulation or missing security features can slip by, especially when falsified documents sit next to legitimate data.

Legacy systems also limit consistency. Without automated systems or a shared structure, teams compare sample documents across folders, emails, and tools.

That fragmentation raises operational costs and makes it harder to uncover fraud early.

This is not about reviewer skill. The breakdown happens when manual processes stretch too far, increasing exposure to financial crime and potential legal consequences for businesses applying for loans and the financial institutions reviewing them.

How Clean File Structure Supports Document Fraud Detection

A clean file structure gives teams a clearer view of what they are reviewing.

When business loan files follow the same order, it becomes easier to compare original documents, spot gaps, and question illegitimate documents without rushing.

Early organization helps reviewers focus on judgment, not sorting. Bank statements, business owner IDs, business registration records, and other records sit where teams expect them.

That consistency helps uncover fraud patterns tied to document forgery or serial fraud, without relying only on specialized tools.

Structure also supports teamwork. Clear files make training simpler, reduce back and forth, and lower the risk of missing context that could carry legal implications for businesses applying for loans.

This approach does not replace human decision-making. It gives reviewers the space to apply experience, use visual checks, and rely on supporting signals like historical records or metadata analysis when needed.

How to Handle Document Fraud at Scale

As submission volume grows, it’s better to rely on a repeatable structure rather than one-off fixes or manual workarounds. Handling document fraud at scale means setting clear rules for how business loan files enter, move, and reach review.

Here are a few practical steps:

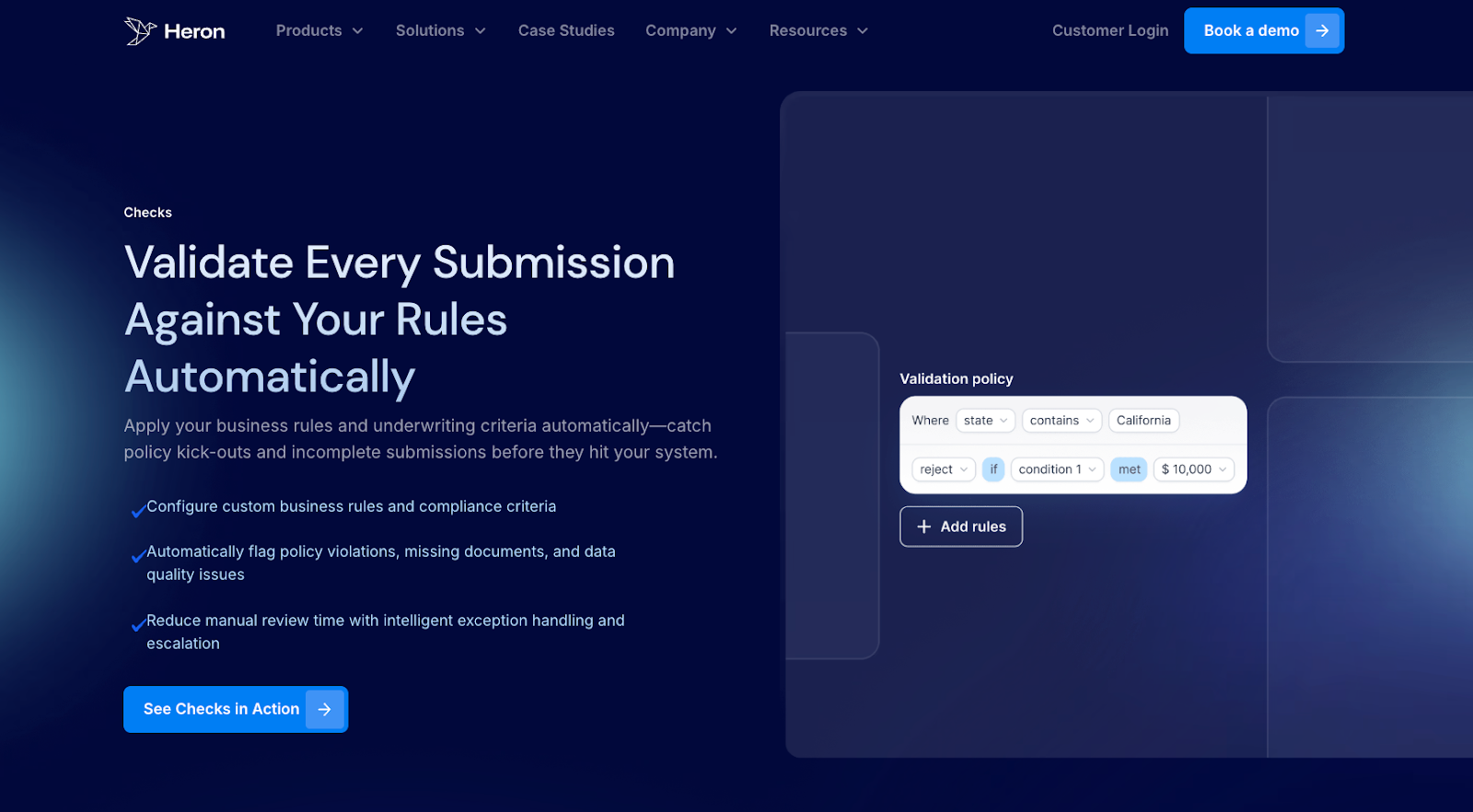

- Standardized intake across submissions - Every business file enters through a defined intake path, with missing items flagged before review begins.

- Clear document grouping by file type - Bank statements, IDs, and supporting records stay in fixed sections. This helps reviewers compare files faster and notice missing security features.

- Early verification and consistency checks - Basic checks compare names, addresses, totals, and financial data across documents before files reach credit review.

- Reliable handoffs to credit teams - Clean files move forward without rework. That reduces delays, supports document fraud prevention without slowing business funding.

How Heron Supports Document Fraud Review

Heron supports document fraud review by fixing the part that usually breaks first: messy files and inconsistent intake.

When business loan submissions arrive through emails, portals, and ISOs, Heron steps in to scrub and organize files before review starts.

Bank statements, applications, IDs, and supporting documents are grouped correctly and organized into a consistent structure that your team can use in your system of record.

This matters because a clean structure cuts the time it takes to understand what belongs together.

You can compare documents faster, notice mismatches earlier, and spend less time opening PDFs just to understand what you’re looking at.

Heron can surface missing information and consistency issues, based on the rules you set, so obvious issues surface before credit review.

Importantly, Heron does not replace human decisions. It prepares review-ready files, supports KYB checks, SOS checks, and web presence analysis, and gives you a clearer context when fraud risk appears.

FAQs About Document Fraud

What constitutes document fraud?

Document fraud involves submitting altered, forged, or misleading documents as part of a business loan application. This can include changing figures, reusing documents in the wrong business context, or submitting scans that lack other security features commonly used to confirm authenticity. These actions aim to mislead reviewers and can make it harder to detect fraud during standard review.

What are the three types of document fraud?

The three common types of document fraud are document alteration, document forgery, and misuse of genuine documents. In business funding, this often includes edited bank statements, reused templates across submissions, or real documents tied to the wrong business, sometimes linked to activity reviewed by government agencies.

Is document fraud a crime?

Yes. Document fraud is a financial crime. Submitting false or manipulated documents can carry serious legal consequences, including fines and prosecution, especially when it involves putting businesses or financial institutions at risk through false information.

What is an example of a document symptom of fraud?

A common document symptom of fraud is inconsistent totals across files or missing security details in scanned PDFs. Review teams may also notice repeated layouts across submissions or text that becomes easier to compare after optical character recognition converts a scan into searchable text, which may require forensic support to review more closely.