When businesses apply for loans, the first thing funders and brokers see is the file. If that file comes in incomplete, unclear, or inconsistent, everything slows down.

Teams spend time chasing missing documents, checking the same details twice, and fixing issues that should have been caught earlier.

Lending verification helps bring order to that first review. It gives MCA funders, brokers, and insurance teams a clear way to confirm business information, review documents, and spot issues before underwriting starts.

When verification stays structured, teams handle more submissions each day without lowering review quality.

This article breaks down how funders and brokers approach lending verification in a clear, step-by-step list.

TL;DR

- Lending verification helps MCA funders, brokers, and insurance teams review business loan applications faster and with fewer errors.

- Best practices include starting with a clean intake, running early identity checks, confirming business income, and reviewing bank account activity and assets.

- Teams should look at credit patterns and risk signals early, then keep every file structured the same way to avoid delays.

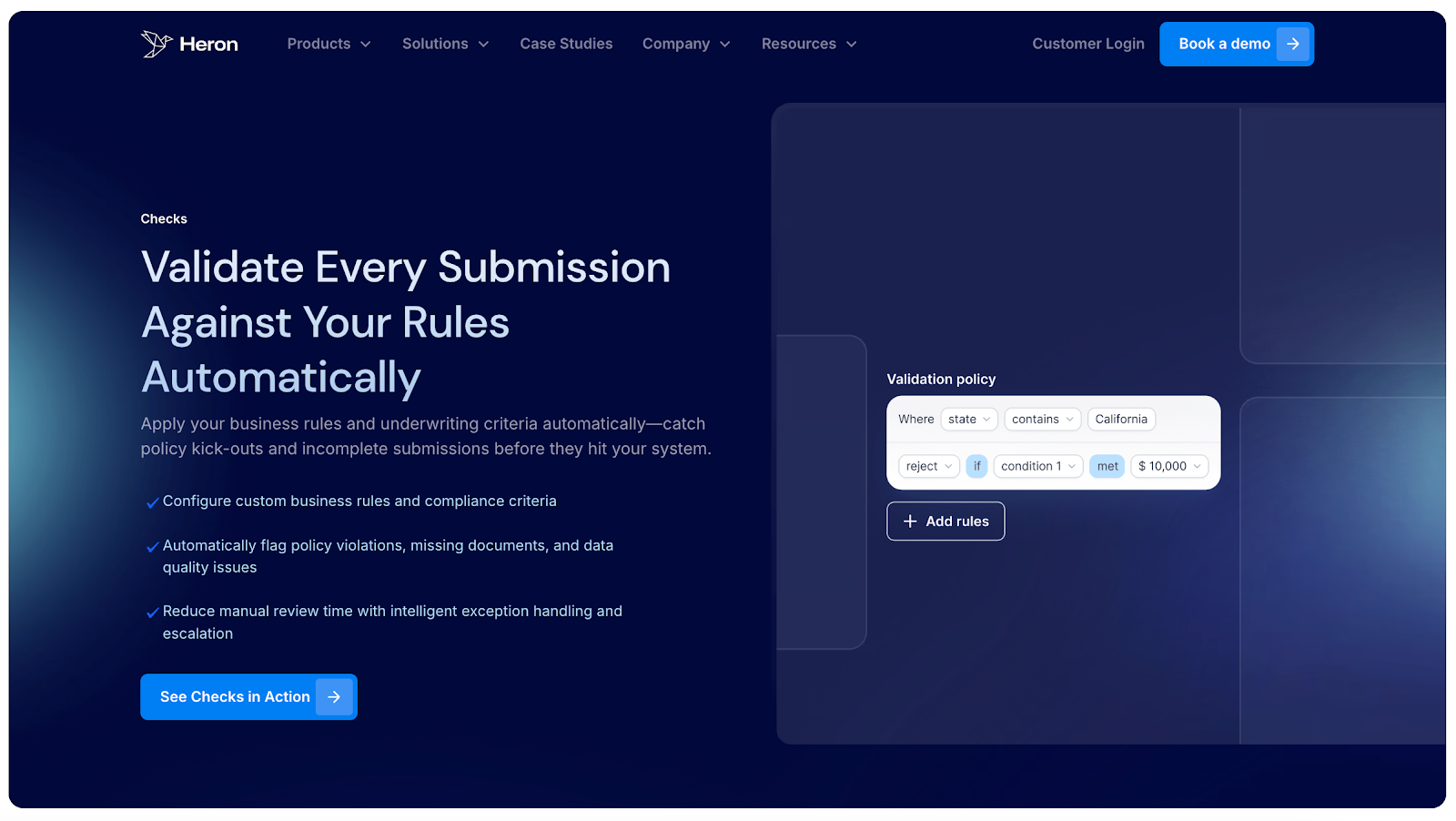

- Tools like Heron remove manual prep work by scrubbing documents, structuring submissions, and flagging issues before underwriting starts.

How Funders and Brokers Run a Strong Lending Verification Process

A strong lending verification process follows a clear order. Funders and brokers start by getting clean information, then confirm key details before underwriting begins.

The steps below show how teams review business loan files in a consistent way that reduces delays, limits follow-ups, and keeps reviews moving.

1. Start With Clean Information

Lending verification begins as soon as a business submits its application. When forms come in incomplete or details change from one file to the next, funders and brokers lose time fixing issues instead of reviewing deals.

Clean business applicant information means using clear forms, asking for the same details every time, and limiting free-text fields where data can vary.

When businesses provide complete information upfront, teams spend less time following up for proof, signatures, or missing documents. This improves accuracy and helps files move through the lending process without added costs.

2. Identity Verification Should Happen Early

Identity verification works best when it happens early in the review. For business loans, this step helps confirm who is behind the application and reduces exposure to identity fraud before deeper checks begin.

Funders and brokers often review business owners, signers, and related entities at a high level. The goal is not to slow the deal, but to spot issues that could block approval later.

Some teams may reference methods like biometric authentication, but the focus stays on confirming identity and protecting the file, not adding friction or delaying the review.

3. Confirm Income and Employment for Business Loans

Income verification looks different for businesses than for individuals. Instead of relying on a single paycheck, funders focus on income and revenue proof to understand how the business earns, pays expenses, and stays stable over time.

This usually means reviewing bank statements, financial statements, and tax records filed with the IRS to confirm cash flow and revenue patterns. These documents give a clearer picture of whether the business can support repayment under the proposed loan terms.

In some cases, employment details may still matter for owners or guarantors. When that applies, some teams reference third-party sources like The Work Number, but this is not standard across all MCA workflows.

What matters most is confirming business income and revenue consistency, not verifying traditional W-2 employment.

4. Review Assets and Business Bank Account Activity

Assets and bank account activity help funders understand how a business operates day to day. Reviewing this information shows whether the business has enough cash on hand and steady movement to support a loan.

This step often includes looking at recent bank account activity, incoming payments, and available assets the business can access if needed.

When this information is complete and easy to review, teams can move faster and spot a fraudulent document before it causes delays.

Clear asset data also supports better approval decisions and helps avoid delays later in underwriting.

5. Check Credit and Reports for Risk Signals

Credit reviews work best when teams focus on patterns instead of single numbers. For business loans, funders look for signs that show how the business handles obligations over time.

High-risk signals can include missed payments, sudden changes, or gaps in reports. A simple risk-based approach helps teams select which files need closer attention and which can move forward toward a faster credit decision.

Spotting these signals early protects the deal and keeps the process from stalling near the approval stage.

6. Keep Verification Consistent Across All Files

Consistency plays a crucial role in lending verification. When every submission follows the same structure, teams spend less time interpreting files and more time reviewing them.

Using the same forms, required fields, and document order across a variety of submissions improves efficiency and reduces judgment calls.

It also helps underwriting teams review files with confidence, since each file provides the same type of access to information.

7. Reduce Back and Forth With Borrowers

When businesses apply for loans, repeated requests slow everything down. Each follow-up adds time to the lending process and pulls teams away from active reviews.

Clear requirements up front reduce the number of messages needed to complete a file. When funders select the right information early and review it in real time, decisions move faster.

This approach benefits both teams since fewer requests lead to quicker answers and less confusion during the review.

8. Prepare Review Ready Files for Underwriting

A review-ready file gives underwriting teams everything they need in one place. It includes complete documents, clear data, and the right order for review.

When files reach underwriting in this state, teams work more efficiently and avoid rechecks that delay approval. Review-ready submissions also help files move toward being approved without extra handoffs or missing details.

The result is a smoother review and a faster path to a decision.

How Verification Services Reduce Manual Work for Funders and Brokers

Verification services help funders and brokers spend less time fixing files and more time reviewing business loan submissions. Instead of chasing other information or correcting small issues, teams work from cleaner data from the start.

These services support faster reviews by:

- Connecting documents and data into one clear file

- Reducing errors that slow down underwriting

- Making it easier to access key details without repeated requests

When teams implement the right technologies, they improve speed without changing how they review risk. Fewer manual steps also create a smoother experience for businesses applying for loans, since requests stay clear and limited.

Using shared resources across teams keeps reviews efficient and helps submissions move forward with less friction.

Speed Up Lending Verification Reviews With Heron

High-volume MCA funders, brokers, and insurance teams deal with the same issue every day: business loan files arrive messy, incomplete, and inconsistent.

Teams spend time opening PDFs, scrubbing bank statements, checking details, and moving information into their CRM before underwriting even starts.

Heron supports lending verification by handling that prep work automatically, so teams can review business applications sooner.

Heron helps teams process hundreds of business loan submissions each month without adding headcount.

MCA funders using Heron report that underwriting teams no longer spend time on data entry. Submissions arrive organized and verified, which lets teams focus on approving deals and sending offers faster.

How Heron helps with lending verification:

- Scrubs documents and data so bank statements, applications, and financial documents arrive clean and ready to review

- Structures submissions for review by turning emails and attachments into organized, consistent records inside your CRM

- Supports underwriting teams by flagging missing data and surfacing key details before review starts

- Runs SOS checks to spot early risk signals in business submissions

- Performs KYB checks to confirm business entities before deeper review

- Uses web presence analysis to validate business activity beyond submitted documents

- Adds instant court research to surface legal signals without manual searches

Heron fits directly into your existing system of record and focuses on MCA and small business lending workflows, not generic automation. Teams move faster because verification work happens before underwriting touches the file.

FAQs About Lending Verification

What is lending verification?

Lending verification is the process funders and brokers use to confirm key information in a business loan application. It focuses on checking business details, documents, and risk signals before underwriting starts, so teams can review files with confidence and avoid issues later in the lending process.

How to verify if a lending company is legit?

To verify if a lending company is legit, businesses can check business registration details, look for a clear web presence, review contact information, and confirm licensing where required. Funders and brokers often rely on trusted data sources and internal checks to ensure the company operates as claimed before moving forward.

What does the verification process include?

The verification process includes reviewing business information, confirming identity details, checking income and assets, and looking for risk signals in credit or reports. For funders, this step helps organize submissions and prepare files for underwriting without jumping into a full review too early.

How does lending verification differ for mortgage lenders and business loan funders?

Lending verification differs for mortgage lenders and business loan funders based on speed, data depth, and review focus. Mortgage lenders usually follow stricter rules and longer checks, with more documents and formal reviews. Business loan funders focus on faster decisions, cash flow, and day-to-day business activity, using lighter checks to move files to underwriting sooner.