Underwriting business loan applications takes more time than it used to. Not because the decisions are harder, but because the prep work keeps growing.

Teams now handle large volumes of submissions from businesses applying for funding. Each application comes with bank statements, financial documents, and supporting files. These files often arrive messy, incomplete, or named at random.

Before any real risk assessment begins, human underwriters spend hours sorting documents, checking details, and fixing gaps in the underwriting process.

This is where AI underwriting starts to show real value. Not as a replacement for experience or judgment, but as a way to remove friction from early review.

Instead of relying on traditional approaches that slow teams down and increase human error, artificial intelligence helps prepare submissions so underwriters can focus on making decisions faster.

In this article, we walk through how AI supports business loan underwriting, where it removes manual work, and how Heron helps teams review applications more clearly and faster.

TL;DR

- AI for underwriting helps teams prepare business loan submissions faster without replacing human judgment.

- It reduces manual prep by organizing files, scrubbing bank statements, and flagging issues early.

- Underwriters spend less time fixing paperwork and more time reviewing real risk.

- AI supports consistency and speed across high-volume insurance and lending workflows.

- Tools like Heron help MCA brokers and funders handle more deals without adding staff.

What AI for Underwriting Really Means in the Insurance Industry

AI for underwriting in the insurance industry works as a support layer for teams reviewing commercial submissions and business funding applications. It helps prepare submissions before anyone starts making decisions.

Instead of reading every document from scratch, underwriting AI organizes files, pulls key data points, and turns unstructured data into something teams can review quickly.

This early data collection step improves risk assessment accuracy without changing how underwriters apply judgment.

AI does not approve or decline applications. It supports decision-making by giving underwriters cleaner inputs, clearer context, and accurate responses based on reliable data sources.

Strong human oversight stays in place to meet regulatory compliance needs and maintain fairness across decisions.

Underwriters gain clearer analysis and stronger decision justification, while staying in control of every outcome.

Why Underwriting Teams Are Adopting AI

Underwriting teams now handle large volumes of business applications across funding, insurance policies, and property coverage. Manual review does not scale well when submissions keep coming in.

Small issues add up fast. Retyping numbers leads to human error. Missing documents slow reviews. Inconsistent checks create challenges for insurance companies trying to maintain compliance and deliver a consistent experience.

AI helps automate routine tasks like document checks, rule validation, and early fraud detection. These AI solutions allow teams to analyze thousands of records faster and improve underwriting efficiency without cutting corners.

Faster reviews help insurance companies respond sooner, support better customer experiences, and maintain competitive pricing, while underwriting teams spend less time on busywork and more time applying judgment to real risk.

Where AI Supports the Insurance Underwriting Process

AI supports the insurance underwriting process at specific stages where manual work slows teams down. These steps happen before any decision is made, while submissions are still being sorted, checked, and prepared for review.

This is where AI has the biggest impact for insurers handling business applications.

Submission Intake and File Organization

As business applications arrive, AI sorts documents right away. It renames files based on their content, groups related documents, and links everything to the correct case.

Underwriters no longer open random PDFs to figure out what belongs where. This gives teams a clear view of each submission and keeps reviews moving without guesswork.

Preparing Data From Business Documents

Business applications often include bank statements, financial statements, and supporting reports from different systems. AI reads these files and prepares key details in a structured format before review.

Instead of copy-pasting numbers across tools, teams start with prepared data tied to the right case. This reduces mistakes and keeps reviews consistent, even as applications grow more complex.

Early Submission Checks

Before the review starts, AI checks for missing files and basic rule issues. These checks support underwriters by stopping weak submissions early.

Fewer back-and-forth emails mean faster decisions, shorter turnaround time, and better customer satisfaction.

Surfacing Early Risk Signals

AI helps surface issues early by reviewing submissions for patterns that often slow reviews or lead to declines. This includes missing information, inconsistencies across documents, and signals that suggest a submission needs a closer look.

Instead of finding these problems midway through the review, underwriters see them up front. Fraud signals, eligibility gaps, and unusual details stand out early, before time is spent on deeper analysis.

Underwriters keep full control, but they start each review with a clearer context and a stronger ability to focus on what is crucial.

How AI and Underwriters Work Together

AI works best when it handles the heavy prep work, and underwriters focus on judgment. This split helps insurers move faster without losing control or transparency in decisions for business applications.

What AI Handles Well

AI takes on tasks that slow teams down during early review. It checks large document volumes, applies standard rules, and keeps files consistent across cases. These steps improve transparency because every submission follows the same structure and checks.

For underwriting teams, this brings clear benefits, especially when applications arrive in bulk from brokers or partners.

AI also helps prepare cases so underwriters can explain decisions clearly later, which matters when businesses ask for context around pricing or terms.

What Underwriters Do Best

Underwriters focus on what AI should not touch. They review exceptions, apply experience, and make final approval decisions for businesses applying for funding.

Human judgment plays an important role when evaluating risk tradeoffs, setting personalized policies, or deciding whether a deal makes sense as an attractive offer for both sides.

AI supports the process, but underwriters stay accountable for outcomes and relationships.

Heron: Helping Underwriters Start With Clean Files

Heron helps MCA brokers, funders, and insurance teams handle more business applications without adding headcount. It focuses on the messy work that slows down underwriting before real decisions happen.

Heron steps in as soon as a submission hits your inbox and prepares what your team needs to review a deal with confidence.

Prepares Review-Ready Submissions

Heron accepts applications from shared inboxes, portals, or APIs and organizes everything by case. Files get renamed, grouped, and routed automatically, so underwriters stop chasing attachments and start reviews with a full picture.

Scrubs and Structures Data

Heron handles bank statement scrubbing and other financial documents, pulling out the details teams actually use. Instead of manual entry, underwriters review structured data that is ready for decision-making.

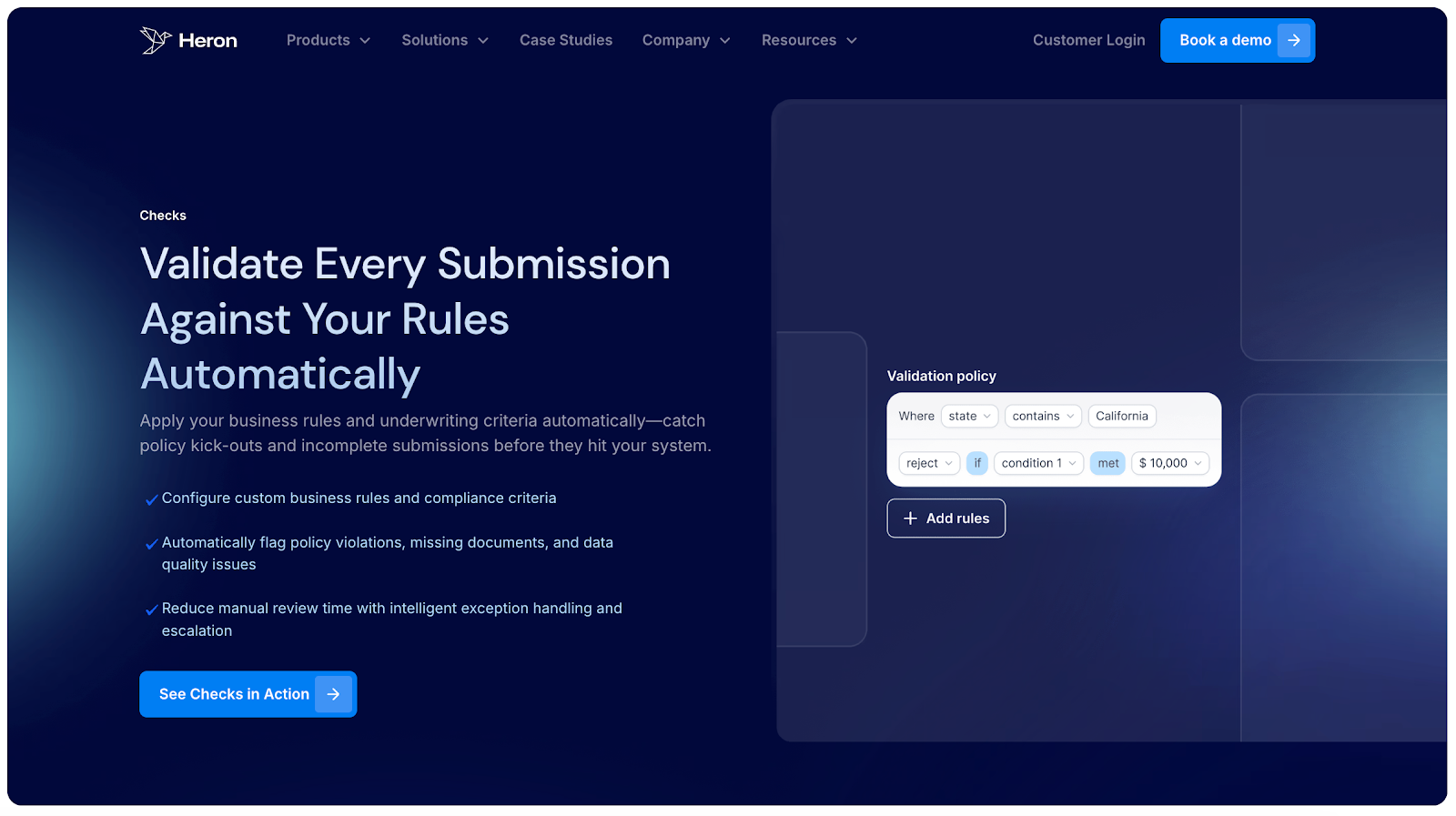

Applies Your Underwriting Rules

Heron runs checks against your rules before the review starts. This includes appetite screens, missing data alerts, and newer checks like SOS verification, KYB checks, web presence analysis, and instant court research.

Weak submissions get flagged early, before they clog the queue.

Flags Issues Before They Become Delays

Fraud signals, inconsistencies, and gaps surface upfront. Underwriters keep control, but they spend less time hunting for problems and more time reviewing real opportunities.

What This Looks Like in Practice

Family Business Funding provides merchant cash advances to small businesses and handles a high volume of submissions every day. Before Heron, manual data entry and bank statement review slowed their underwriting team down.

After adopting Heron, they cut time-to-offer by 50% and freed up two full-time roles previously focused on data entry.

⭐⭐⭐⭐⭐

“Heron has eliminated the data entry phase of our underwriting process. We now have a clear picture of revenue, positions, and the legitimacy of the file within minutes of the submission email.”

-Valeria, Managing Director, Family Business Funding

With cleaner files and faster prep, underwriters moved through reviews with greater confidence and sent offers out much earlier.

FAQs About AI for Underwriting

How can AI be used in underwriting?

AI is used in underwriting to prepare business loan applications before review. It helps organize submissions, scrub bank statements, check for missing information, and flag early issues. This allows underwriting teams to focus on risk review and decision-making instead of manual prep work.

Will underwriting be taken over by AI?

No. Underwriting will not be taken over by AI. A human underwriter remains responsible for reviewing risk, handling exceptions, and making final approval decisions. AI supports the process by reducing manual work, but judgment and accountability stay with people.

How can generative AI contribute to loan underwriting?

Generative AI models contribute to loan underwriting by helping organize and summarize large volumes of business documents. They can highlight key details, group related files, and prepare submissions for faster review. Generative AI supports underwriters with cleaner inputs, but it does not replace human decision-making.

How do machine learning algorithms support risk review in underwriting?

Machine learning algorithms support underwriting by spotting patterns across submissions that are easy to miss during manual review. They help flag inconsistencies, unusual activity, and risk indicators across business documents, including submissions tied to commercial property or casualty coverage. These signals guide underwriters to areas that need closer attention, while final decisions remain human-led.