Underwriting has always been one of the most time-consuming parts of the insurance process.

Manual reviews, endless data entry, and slow approvals frustrate both underwriters and customers. When applications pile up, costs rise, and opportunities are lost because teams cannot respond quickly enough.

Automation in underwriting can help solve this problem. In this guide, we will walk through what automation in insurance underwriting looks like, what drives the adaptation of automation, and more.

What is Automation in Insurance Underwriting?

Automation in insurance underwriting means using advanced technology to handle tasks that once required hours of manual work.

With tools like artificial intelligence, machine learning, and natural language processing, insurers are automating processes that collect, analyze, and validate large sets of data.

They can also use intelligent document processing (IDP) and optical character recognition (OCR) to pull information directly from forms, applications, and other documents without the need for manual entry.

Automation can also apply underwriting rules with speed and consistency. Manual reviews often take time and leave more room for error, while insurance underwriting automation processes the data quickly and delivers clear insights to guide decisions.

Automation for insurance also supports compliance by making sure underwriting rules are applied the same way every time. The result is quicker policy approvals, fairer pricing, and a smoother experience for both insurers and customers.

Types of Automated Underwriting Systems

Automated underwriting systems don’t all work the same way. Each system has its strengths, and many companies use a mix to improve efficiency, accuracy, and customer satisfaction.

Rules-Based Systems

Rules-based systems rely on clear business rules to make decisions. These follow “if-then” logic to process applications.

For example, a managing general agent (MGA) focused on fleet coverage could set rules that automatically approve submissions for fleets under five vehicles with no loss history in the past three years.

The system applies the pre-set conditions and passes qualifying submissions straight through to binding.

This approach works best for straightforward applications that involve low-risk profiles. It’s a reliable option for repetitive cases, freeing up insurance agents to focus on more complex applications or existing clients.

While it lacks flexibility, it delivers fast decisions and helps reduce backlogs in the underwriting department.

Predictive Model Systems

Predictive model systems apply statistical methods and predictive analytics to evaluate risk. They use large sets of historical data to estimate the likelihood of events like claims or fraud.

Predictive models are especially valuable for managing general agents when evaluating long-term risk exposure across specialized lines like cyber liability, fleet, or commercial property.

The system can score submissions based on patterns from thousands of past accounts, giving underwriters a clearer view of how risks may perform over time.

For example, a predictive model in a cyber liability MGA might assign a higher risk score to a business in the healthcare sector with outdated security controls, while a tech firm with a strong history of compliance receives a lower score.

This allows the MGA to act quickly with data-driven insights that support smarter underwriting decisions and more accurate pricing, while maintaining strong carrier relationships.

Predictive models also support underwriters by flagging risks that look profitable versus those likely to generate losses, helping MGAs focus their time where it matters most.

Machine Learning Systems

Machine learning systems go further by using advanced analytics to spot complex and often hidden patterns in the data.

Unlike rules-based or predictive models, machine learning improves over time as it processes more information.

For insurers, machine learning systems can adapt quickly to new data, such as changes in health trends or shifts in claim behavior.

While these systems require significant resources to set up and maintain, they bring flexibility and accuracy that lead to stronger risk management and higher customer satisfaction.

Hybrid Systems

Hybrid systems combine business rules, predictive models, and machine learning into one framework. Submissions are routed to the right system depending on their complexity and the data available.

This might mean a small commercial property account with no loss history passes through a rules-based check, while a high-risk cyber liability case is sent to a machine learning system for deeper analysis.

This blended approach gives MGAs the best of both worlds: speed for routine submissions and advanced analytics for complex risks.

It allows them to handle more volume, maintain pricing accuracy, and respond quickly to retail agents who expect quotes within hours.

Underwriters also benefit from hybrid systems because they can focus their time on negotiations and complex cases while the technology handles repetitive data review and routing.

3 Key Reasons Driving the Use of Automation in Insurance Underwriting

Automation is becoming a core part of how insurers handle underwriting. But why? Here are three key reasons why automation is gaining so much ground in insurance underwriting.

1. More and More Insurers Adapt AI Technologies

Market trends show a clear shift in the insurance industry from manual underwriting to automated insurance underwriting processes.

According to an article published by the Risk & Insurance Editorial Team, about 61% of insurers used artificial intelligence in their workflow in 2023. By 2024, the same report shows that the number rose to 77%, showing how quickly AI-powered tools are becoming part of daily operations.

The report also points out that artificial intelligence is making insurance sales and underwriting more accurate and efficient.

AI algorithms can review large amounts of relevant data, including customer details and outside factors, improving risk assessment accuracy and giving insurers a clearer view of potential exposure.

With this support, automated insurance underwriting processes move faster and reduce errors linked to repetitive tasks that often slow down manual underwriting. This allows underwriters to focus more on cases that need human judgment.

And the momentum for this adaptation is set to grow even stronger. A different report by Coinlaw shows that by 2025, 83% of insurance executives were expected to make AI a top priority in their digital transformation strategies.

2. Insurers See Improvements in Cycle Times with Automation

Slow underwriting and complex forms have long been a frustration. Automated underwriting solutions change this by simplifying how information is collected and speeding up the entire process.

Companies that invest in automation see clear improvements in underwriting productivity. A study by McKinsey shows insurance cycle times can be cut by 50% to 70%.

Another report by Convin.ai highlights that insurers using intelligent automation in insurance achieve 40% faster cycle times in policy administration.

These two findings show that automation can make the underwriting department much more efficient. Faster decisions mean fewer delays for customers, smoother onboarding, and a better overall experience.

Onboarding that once felt drawn out can now be completed in a fraction of the time, giving customers a smoother path to getting covered.

With better and easier handling of both structured and unstructured data, underwriting departments can now make informed decisions much faster, with fewer underwriting errors, and insurance policies get issued with less hassle.

For insurers, automation means less time spent on repetitive tasks, fewer underwriting errors, and stronger cost savings across the business.

3. AI Strengthens Fraud Detection in Underwriting

Fraud detection has become one of the biggest areas where automation is making a difference.

According to BirlaSoft, AI-powered underwriting systems now improve risk assessment accuracy by up to 25%, and some algorithms catch fraudulent claims with accuracy rates above 90%.

For human underwriters, this kind of support makes the job easier. Underwriting process automation can flag unusual patterns or risk factors that would take hours to find in a manual review.

With the basics handled, underwriters can spend more time on cases that need judgment while still following their underwriting guidelines.

This shift also ties closely to risk management. Fraud not only hurts profits but can also slow down the underwriting process.

When policy administration systems bring AI into the workflow, fraud checks happen quickly and smoothly as part of daily operations, supporting more accurate and consistent underwriting decisions.

How Can You Get Started with Automating Your Insurance Underwriting Process?

Moving from traditional processes to automation requires planning. Your goal shouldn't be to replace underwriters, but to free them from repetitive manual tasks and help them focus on higher-value decisions.

Here’s a step-by-step look at how to get started.

Assess Your Current Underwriting Workflows

The first step is to understand how your underwriting department works today. Map out the full process, from application intake to policy issuance.

Look for bottlenecks like manual document processing, back-and-forth emails, duplicate data entry, and long approval chains.

For example, if underwriters spend hours retyping business details from scanned forms, that is a clear sign that automation can save time.

Spotting these pain points gives you a roadmap for where automation will create the most impact.

Identify and Consolidate Data Sources

Automation is only as good as the data it uses. Insurance companies often have valuable information scattered across multiple systems, such as CRM platforms, claims history, or internal policy files.

Adding external sources like fleet telematics, commercial credit reports, or property inspection data builds a fuller picture of business risk.

For example, telematics can help assess the safety profile of a company’s fleet, while credit and inspection data can highlight exposure in commercial property accounts.

When combining these data points, MGAs should prioritize security and compliance to protect sensitive business information and maintain carrier confidence.

Choose the Right Automation Platform

Not every platform will fit the unique needs of insurance companies or funders. The best choice is one that supports rules-based decisioning, predictive modeling, and machine learning while also connecting seamlessly with your current tools.

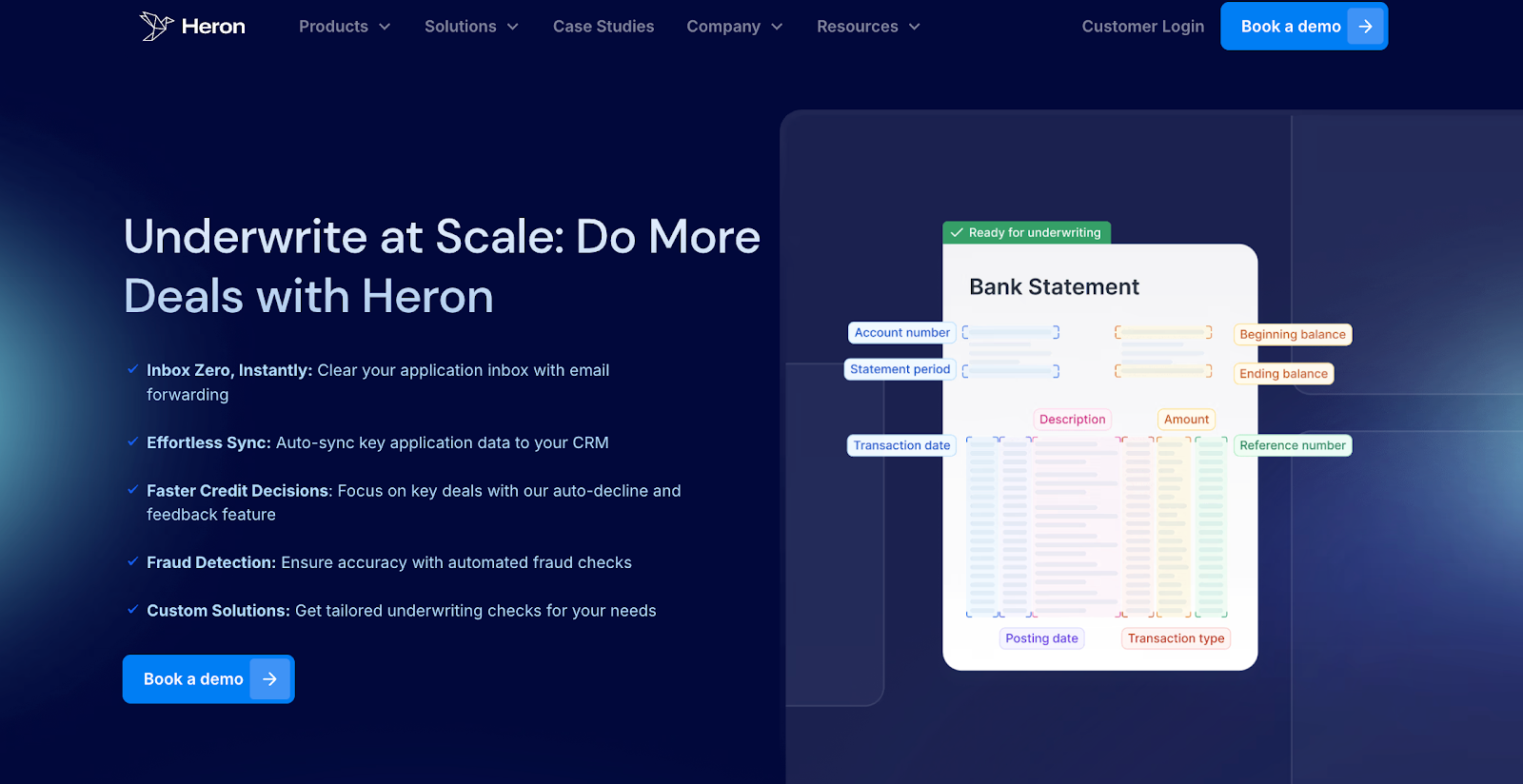

Heron stands out as an insurance automation platform. It is built to help high-volume MCA funders and insurance brokers scale without adding headcount.

The platform automates some of the most time-consuming parts of the underwriting process, including application intake, business bank statement analysis, and funder decision emails. All of this happens in seconds, with clean, structured data pushed directly into your CRM.

With features like auto-decline for faster credit decisions, inbox clearing through email forwarding, and automated fraud checks, Heron makes automated underwriting in insurance practical and easy to adopt.

Book a demo to learn how you can do more deals with Heron!

Run a Pilot and Optimize Results

Start small with a pilot project before rolling automation out across the entire team.

Some MGAs and other financial institutions test automation on lower-risk commercial accounts, such as cyber submissions for small professional firms with strong security controls, or standard property risks under a set insured value with no recent loss history.

Others may pilot automation on package policies for main street businesses, where the exposures are predictable and the carrier appetite is clear.

During the pilot, track metrics such as turnaround times, accuracy of risk scoring, and how well the system applies delegated underwriting rules. These insights help refine AI models and decision logic so the process fits the MGA’s operations.

Over time, this leads to stronger risk management, faster quotes for retail agents, and greater confidence from carrier partners.

Simplify Your Insurance Underwriting Process With Heron

Heron helps insurers move past the limits of legacy systems by bringing intelligent automation into everyday underwriting.

Instead of losing time to messy inboxes and endless rekeying, Heron connects to multiple data sources and turns unstructured submissions into clean, structured data.

The result is less time wasted on reducing manual effort and more time spent on underwriting. With Heron, teams can respond to submissions in hours, not days, cut processing costs by over 75%, and scale volume without adding headcount.

If your team is buried in submissions and struggling to keep up, Heron is built for you.

FAQs About Automation in Insurance Underwriting

What is the automated underwriting process?

The automated underwriting process uses software to review financial and personal data, then makes quick loan or insurance decisions without long manual checks.

It speeds up approvals, reduces errors, and supports straight-through processing, making it easier for companies to keep up with customer expectations.

Will underwriting become automated?

Underwriting is already moving toward automation, especially in areas like mortgages and health insurance, where large amounts of data need quick review. While human oversight will remain for complex cases, more routine decisions are expected to be handled automatically.

What is automation in insurance?

Automation in insurance means using technology to handle repetitive tasks like claims processing, policy setup, and risk checks. It helps reduce paperwork, cut costs, and enhance customer experience by giving faster and more accurate results.

How is AI used in insurance underwriting?

AI in insurance underwriting helps analyze customer data, medical records, and risk patterns with greater speed and accuracy. It supports insurers in pricing policies fairly, reducing fraud, and meeting rising customer expectations for quick and transparent service.