Underwriting is the process of studying and analyzing a business’s financial story to decide if a funding deal fits the risk you are willing to take. It gives you a full view of how the business earns money, spends money, and manages cash flow.

As an underwriter, you look at income, bank activity, credit patterns, past behavior, and the strength of the request. You can handle this work in two ways: by doing a full manual review or by using automation tools that speed up parts of the process.

This article will walk you through what manual underwriting means, its challenges, how automated underwriting compares to it, and more.

What Is Manual Underwriting?

Manual underwriting is when an underwriter looks at a borrower's full financial story. The goal is to understand the borrower's ability to take on the loan and make on-time payments without stress.

A manually underwritten review takes time because it involves underwriters and loan officers studying real documents. You need to manually check bank records, tax returns, and other financial documents that the borrower submits.

You also need to see if they have any past debts, check for potential fraud, and analyze the patterns behind a borrower's spending.

Where Is Manual Underwriting Used?

Manual underwriting shows up in many parts of the finance space. Let's look at where it is commonly used:

SME Lending

Manual underwriting is useful if you want to understand the full picture of the business you are assessing.

Since small and medium companies often have income that shifts with seasons, contracts, or market trends, you need more than a quick look at the top line.

You review bank statements, cash flow patterns, tax filings, and profit statements to see how the business performs month to month and year to year. You also study their plans, current clients, and how money moves through the company.

This helps you judge if the business can manage future loan payments and keep steady operations.

Insurance

In insurance, manual underwriting helps you judge a company's risk profile with care and structure. You look at how a business works, how they deal with their clients, and what choices they make each day.

This includes looking at financial statements, claims history, loss patterns, and any past issues that may affect future exposure.

You need to check how they manage safety, what controls they have in place, and whether their track record supports the level of cover they want.

Mortgage Lending

Manual underwriting in mortgage applications comes up when the case does not fit standard rules. You may choose to follow Federal Housing Administration (FHA) manual underwriting guidelines or other agency rules when the file needs a closer look.

You need to look at a borrower's income proof, pay stubs, past records, and how they handle money. If the borrower has a lower credit score, you need to take extra time to understand the story behind it.

You also need to check if the mortgage payments will fit the borrower's budget. Some files also move through the secondary mortgage market, which means you must keep the manual review clean, complete, and easy to audit.

Consumer Lending

Consumer lending covers personal credit products such as installment loans, cards, and small advances. These cases follow strict rules, and every detail in the file must match the standards you set.

Manual underwriting lets you study each part of the request with care. Many applicants have thin records or irregular activity, and the manual review will help you read the story behind the file. This will help you decide if the request fits the guidelines and if the risk makes sense.

A manual review also makes it easier to keep clean notes, track items that need follow-ups, and stay in line with compliance checks.

The Usual Manual Underwriting Process

Manual underwriting follows a clear path that helps underwriters study the full picture before making a call. Here is how manual underwriting works:

- Submitting all financial documents: You start by gathering the borrower’s full financial information. This includes bank statements, tax returns, and any listed assets.

- Reading through the file: You review past credit accounts, income patterns, and any items that need attention, such as past bankruptcy or open cases.

- Requesting more details when needed: Some files have gaps or unclear areas. You may ask the borrower for missing forms or short notes that explain key points.

- Reviewing risk and fit: At this stage, you check if the borrower can qualify based on income and monthly obligations. The focus is on the debt-to-income ratio. A lower DTI shows more room in the budget, while a higher DTI may require a large down payment to proceed.

- Making the final call: After you study the full file, you decide the next step. You can approve, deny, or request a few more items before you close out the review.

Challenges with Manual Underwriting

Manual underwriting has been a useful tool for a long time, but the manual process comes with real limits. Below are the challenges you face when you manually underwrite files.

Slow Turnaround

A single human review takes time. On average, it takes about 20 minutes for a human to process one submission.

If you are handling thousands of files, this adds up fast. For example, a Secretary of State check is a vital part of the underwriting process.

Each SOS check takes a few minutes, and you repeat it for every application. If you are handling 5,000 loan applications each month, your team can spend more than 250 hours on these checks alone.

And that’s only one part of the work. You still need to go through financial documentation like bank account details and tax records.

Any gaps or unclear entries add even more time. This slows your full pipeline and pushes deals into longer timelines than brokers expect.

Higher Chance Of Mistakes

Manual reviews can miss small details that turn into big problems. A simple typo in income, a missing page, or an incomplete check can cause you to lose thousands of dollars in a failed deal.

For example, when checking if a business has any pending court cases, manual checks usually have a 30% miss rate. This means 1 in 3 lawsuits slips through. With an average cost of $85,000 per missed judgment, the financial hit is serious.

Different Decisions From Different Reviewers

Human judgment changes from one reviewer to another. Two underwriters may read the same case and come to two different conclusions, especially when the borrower has a limited credit history or mixed income sources.

This leads to uneven calls across your underwriting team. A client may notice this and start questioning your standards, which creates more back and forth and longer cycles for each deal.

Hard To Scale During High Volume

When your volume spikes, your team cannot pick up speed. Each underwriter is stuck with the same steps and the same time limits, no matter how many files come in.

You still need to run business verification, read financial documents, and move through all the other review steps one file at a time.

As the queue grows, new files stack on top of older ones. This slows down every deal in the pipeline. Businesses wait longer for answers, and you and your team feel the pressure as the pile keeps growing.

Higher Cost For Your Operation

Manual review requires people, and people cost money. Every file needs someone to read it, check numbers, send follow-ups, and keep notes in order.

Even getting a single loan application into the system can cost $50 or more per file, and that is before the full review even starts. When your volume grows, your staffing needs grow with it, which increases your overhead.

Manual Underwriting vs Automated Underwriting

Manual underwriting may have been what underwriters have used for years, but it's also very time-consuming.

In contrast, automated underwriting systems review income, credit, and other factors through a computer algorithm, helping you make informed decisions and improve underwriting efficiency with less manual work.

Automated tools also help you scale because they handle large volumes without adding more staff. They also cut time by handling tasks that normally take your team several minutes for each file.

Here's a table highlighting the difference between manual and automatic underwriting:

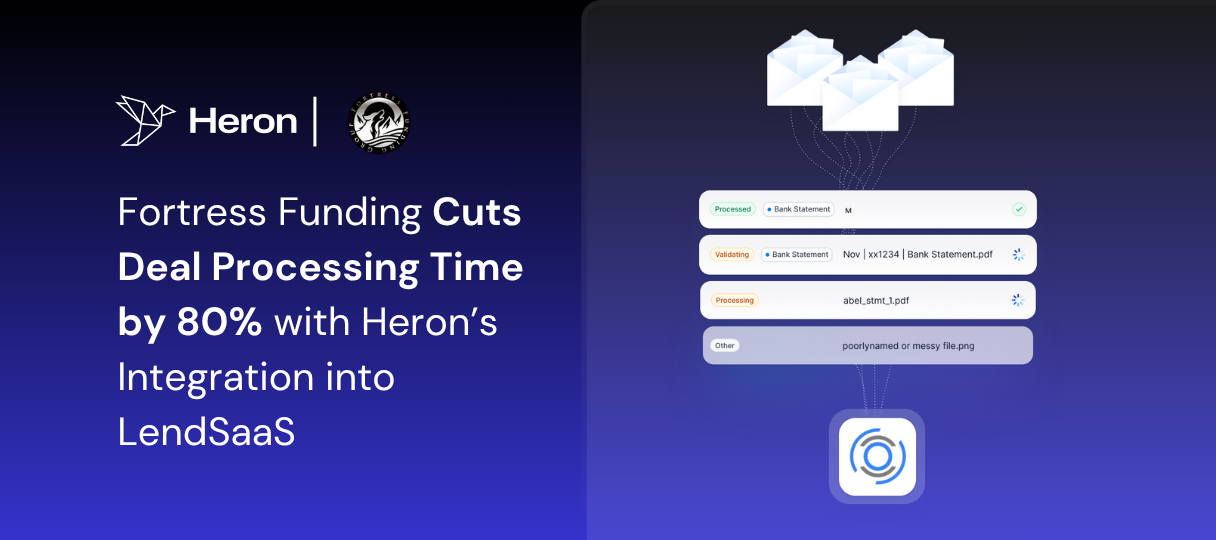

How Fortress Funding Broke Free From Manual Work With Heron and LendSaaS

Fortress Funding was stuck in a tough spot. Each deal started with long hours of manual work. Their team had to open every bank statement, read every line, and key all the data into LendSaaS by hand.

A single file could take an hour or more, and deals piled up faster than the team could process them. Growth was hard because adding more volume meant hiring more staff.

That changed when they brought Heron into their LendSaaS workflow.

Heron now pulls files straight from the submissions inbox, sorts them, reads the bank statements, and sends clean data right into LendSaaS. The shift was instant.

Deal processing time dropped by 80%. Simple deals now take 5 to 10 minutes. Even complex files take only about 30 minutes.

The team no longer spends hours on manual entry. They can handle more deals and bring on more ISOs without hiring new people. Underwriters also get better data thanks to Heron’s anomaly scoring, which helps them spot altered or risky statements early.

See how fast your team could work with Heron. Book a demo today!

Speed Up Submissions Without Adding Staff With Heron

Heron gives you a faster way to move deals from submission to decision without adding more people. It removes the slow steps that hold your team back and gives you clean data you can trust.

This helps you focus on real risk checks. You can see how the borrower handles loan payments, which loan type fits them best, and if the business has any negative marks you need to review.

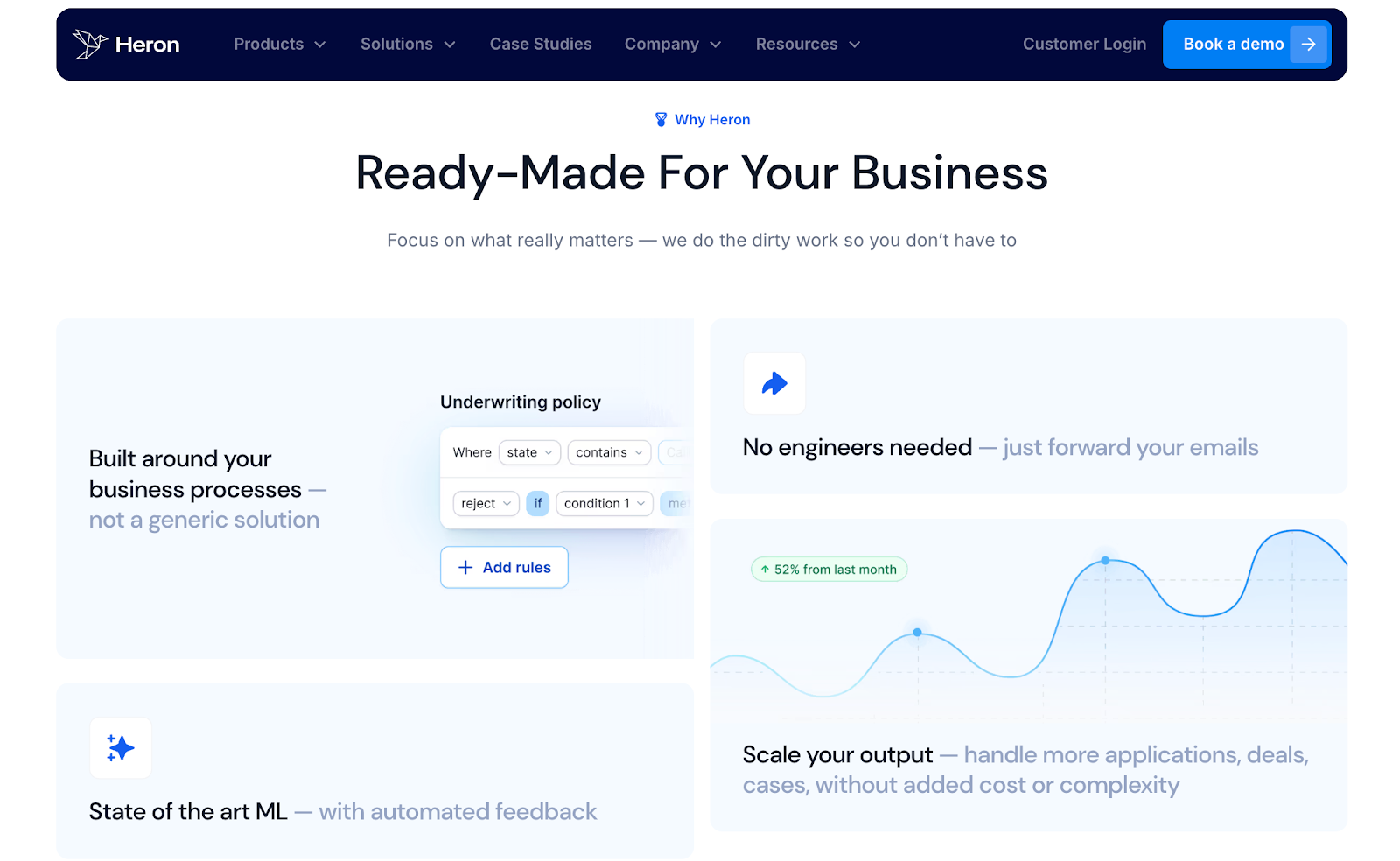

Automate Data Entry And Document Ingestion

Heron pulls full packages straight from email and organizes them for you. This document automation platform reads each file, arranges everything into clean folders, and builds structured records in your system.

Rather than reviewing scattered PDFs, you start with a tidy submission that is easy to navigate. It also captures important numbers from financial documents, which means you spend more time on decisions and less time on setup.

Validate And Enhance Applications

Heron reviews each submission against your underwriting rules as soon as it arrives. It checks required forms, flags issues, and fills gaps using trusted external sources. This gives your underwriters clear, decision-ready data without manually opening long files.

With 99.5% accuracy, you can move faster while still trusting the numbers. It also helps you assess real strengths, like when a borrower's file needs extra context.

Integrates With Your Workflow

Heron works with the systems you already use. It connects to your financial CRM, policy tools, and workbenches, so every step updates in real time.

Records sync automatically, tasks trigger on their own, and you get a full audit trail for every submission.

You do not need a rebuild or a long onboarding cycle. Heron fits into your current setup and keeps your data clean and consistent.

Cut Costs and Save Time

Heron reduces processing costs by more than 75% and shortens response times from days to hours. Teams can handle 2x the usual volume without adding staff, which keeps growth simple and controlled.

The platform supports 50+ document types right out of the box, making it easy to process everything from bank statements to tax files. The outcome is a smoother workflow, fewer delays, and a better experience for every broker in the pipeline.

FAQs About Manual Underwriting

Do banks still do manual underwriting?

Yes, some banks still use manual underwriting, but they usually save it for cases that don’t fit standard rules. It helps when a borrower has a thin credit file or special income details.

What does manual underwriting mean?

Manual underwriting is when you review a borrower's full financial picture with little to no help from automation software.

You look at income, past payments, and debt to decide if a borrower can handle the loan. It’s a slower process, but it gives more room for context that software might miss.

Is manual underwriting hard to get?

It can take more time because the file often needs additional documents or extra notes. Some funders also follow tighter rules for these cases, which can limit what the applicant qualifies for.

Manual reviews are more common in cases that fall outside normal guidelines, such as some jumbo loans, Fannie Mae and Freddie Mac conventional loans, or Veterans Affairs (VA) loans.

What are the cons of manual underwriting?

The main downside is the longer review time and the extra paperwork underwriters need to check. Some deals may also have tighter limits because the business is tagged as high-risk, which may further slow down the process as underwriters need more time to decide.

Another downside is the higher chance of missing small details when everything is done by hand. A simple typo or a missing page can slow the deal or lead to a bad call.