Your day fills up fast when new files keep hitting your inbox. You open one bank statement, then a tax form, then an email from a broker waiting for an update.

Every file feels a little different, and it takes work to keep everything straight. The pressure builds when the queue grows, and the small gaps inside each submission slow your pace.

Many teams feel this pressure. You want to move deals forward, yet the back-and-forth around documents and details can pull you into work that drains time and focus.

A steady workflow helps you stay in control, even when the volume climbs.

If you want a clear picture of how this workflow comes together and how you can keep files moving without the daily drag, this article breaks it down in a way that fits the work you do every day.

TL;DR

- A loan processing workflow guides each file from intake through underwriting and funding, helping MCA brokers and funders stay organized.

- Core steps include intake, early review, cash-flow checks, business verification, credit review, underwriting, terms, and final funding.

- Slowdowns usually come from missing documents, messy PDFs, slow checks, and manual data entry.

- A clear workflow reduces back-and-forth, speeds decisions, and keeps reviews steady across high-volume days.

- Heron scrubs bank statements, runs KYB and SOS checks, flags bad files, surfaces risks, and prepares decision-ready data in seconds.

What Is a Loan Processing Workflow?

A loan processing workflow is the path a file takes from the first touch to the final decision. You move through it every time you review a new submission.

It starts with the loan application process, then carries the file through checks, reviews, and the final loan approval. Each step sits in the same order, which keeps the work steady and helps your team stay consistent.

Most MCA brokers and funders see it as the foundation that keeps the lending process on track.

You look at borrower data, credit evaluation, income statements, and any details tied to existing loans. You use this information to understand the borrower’s creditworthiness and decide if the deal should move forward.

Strong document management supports every part of this workflow, especially when teams want clean files and fewer manual errors.

A clear workflow keeps the day simple for loan officers. It helps you process loan applications with structure instead of guesswork.

Core Steps in a Loan Processing Workflow

Files come in fast, and it helps to have a clear path for each one. Here’s the step-by-step workflow that keeps teams steady even on busy days.

1. File Intake

A new file comes in through the loan application process, and the team gathers the first documents.

Early gaps get flagged, and the file enters the workflow through the same steps used in the loan origination process. This early setup keeps the lending process steady for MCA brokers and funders.

2. Early Review

The team checks whether the file has enough relevant data to move forward. Basic business details, income statements, and key numbers get confirmed here.

Clean information at this stage protects data integrity and removes extra manual loan processing later in the workflow.

3. Cash Flow Review

Cash flow shows what daily life looks like inside the business. Deposits, returns, balances, and trends give MCA funders a quick read on stability.

Many teams use bank statement scanning or scrubbing tools to handle tough PDFs and avoid digging through stacks of pages by hand.

4. Business and Identity Checks

This step makes sure the business is real and active. MCA teams often confirm basic details, check ownership, and look for anything that feels out of place.

Clear information here gives you confidence that the file is safe to move forward. Strong checks at this stage keep your workflow steady and help you avoid slowdowns later in the approval process.

5. Credit and Risk Review

Payment history, credit score, outstanding debts, and credit bureau details help funders understand creditworthiness.

These insights support risk management across lending institutions and prepare the file for the underwriting process, whether handled manually or through automated loan processing tools.

6. Underwriting Review

Underwriters take the scrubbed file and review financial health, business risk, and deal structure.

Some MCA teams lean on underwriting automation or an automation risk assessment tool to improve underwriting efficiency and reduce repeated manual work.

7. Offer and Terms

Once the file reaches loan approval, teams prepare loan terms, repayment schedules, and loan agreements.

This stage brings together numbers, expectations, and regulatory compliance before sharing details with the broker or business owner. It also shapes the start of the loan lifecycle.

8. Final Steps and Funding

Once everything checks out, funding teams complete documentation verification, run final document automation steps, and confirm compliance requirements.

Automated loan management systems help prevent manual errors and keep everything clear. After the file closes cleanly, funds move into the business and enter active loan servicing.

Why a Steady Loan Processing Workflow Helps Teams

A clear, predictable workflow keeps your day from slipping into constant back-and-forth.

When each file follows the same path, your team moves faster and deals with fewer surprises. You get cleaner files, clearer reviews, and decisions that feel easier to make.

Many financial institutions want relief from mixed documents and manual tasks. A steady set of steps creates that relief and removes the small pressures that slow you down.

Automated workflows help teams automate routine tasks that drag out reviews, and they work well with existing systems your team already uses.

This setup supports regulatory requirements and keeps documentation verification simple without adding weight to the process.

A strong workflow supports business growth because it cuts delays across your loan portfolio. Automated systems reduce the need for human intervention, which helps you approve loans with more confidence.

Teams feel the real benefit in their day. Work becomes calmer, decisions land faster, and customers get better support along the way.

Ways To Improve a Loan Processing Workflow

Small changes make the biggest difference in a busy day. A steady workflow helps teams avoid the extra steps that slow reviews and create avoidable pressure.

Here are simple ways to keep files moving:

- Use one process for all files

- Cut extra checks that don’t add value

- Keep documents and data in one place

- Remove manual typing and automate repetitive tasks

- Catch gaps early so you avoid rework later

Tools like loan management software help MCA teams stay organized and support consistent data across other financial systems.

Simple document verification and automated compliance checks reduce compliance issues without adding more work to human resources.

Some teams lean on advanced analytics or credit bureaus to shape decisions throughout the entire process. Automated solutions also lower increasing operational costs and improve operational efficiency.

A strong workflow aids lenders, protects the day from clutter, and gives borrowers better customer satisfaction without adding strain to your team.

Where Teams Lose Time in Loan Processing

Time disappears fast when small issues stack up across a file. Missing documents hold the review in place. Hard-to-read PDFs slow every step, especially when cash flow spreads need a closer look.

Slow KYB or UBO checks add more waiting, and manual data entry makes the day feel heavier than it should.

These delays are common across the financial services industry because teams often work through each problem one file at a time.

Clean information, simple steps, and comprehensive audit trails help, yet many teams still lose time before they even reach interest rates or final terms.

Some teams look at machine learning or other tools, but the real goal stays simple: keep reviews steady and free your team from busywork so they can focus on providing customer support.

If these slowdowns sound familiar, a stronger workflow and the right tools can remove these barriers and keep each file moving with less stress.

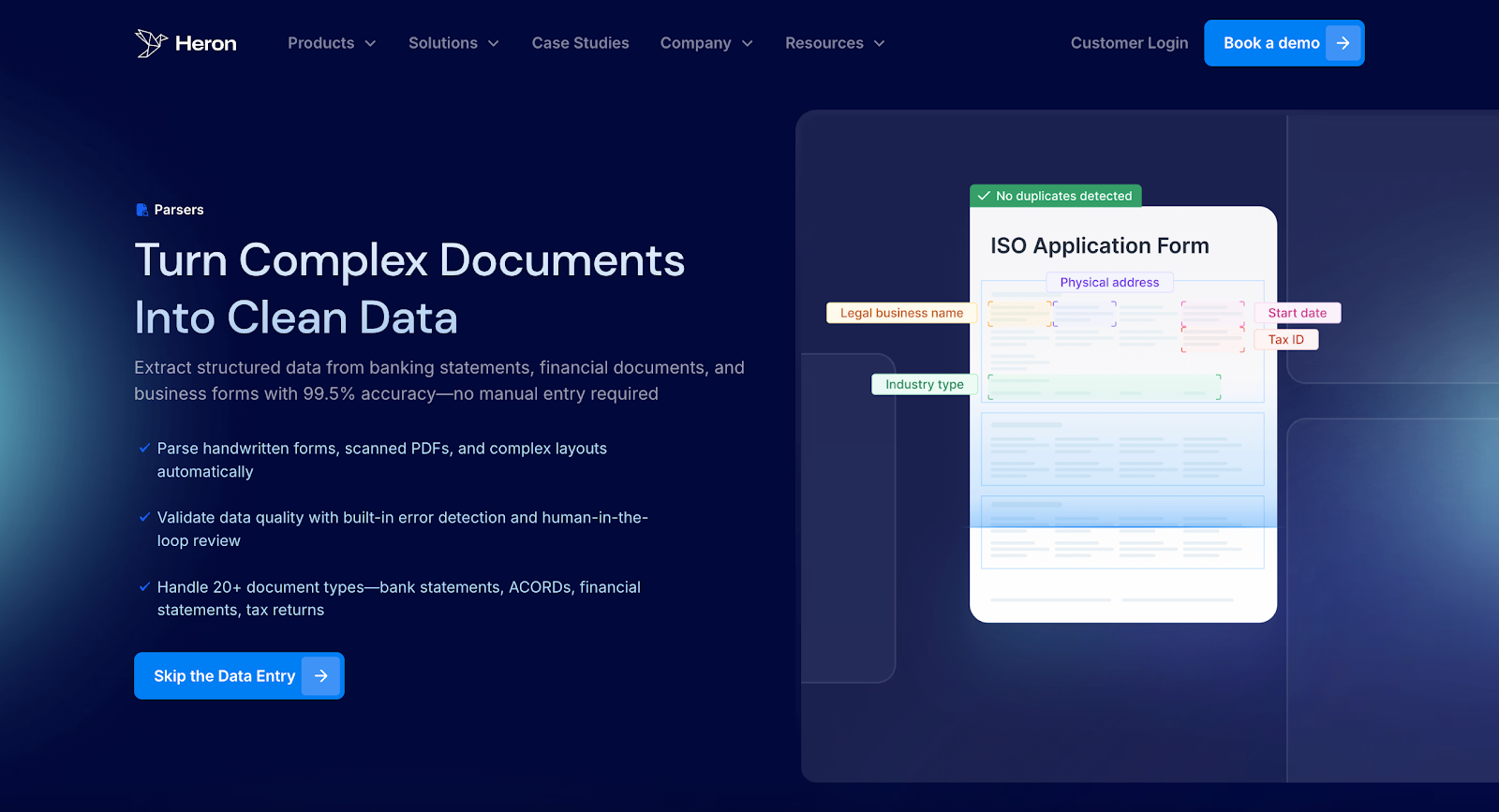

Heron: The Clear Fix for a Messy Loan Processing Workflow

Heron gives MCA brokers and funders a faster and cleaner way to move through every step of the loan processing workflow.

Instead of spending 10–15 minutes scrubbing a single bank statement, your team gets decision-ready numbers in seconds. This clears the back-and-forth that slows deals and keeps underwriters stuck inside PDFs.

More than 130 financial teams use Heron to handle high-volume submissions without adding staff.

The platform fits into your existing system, scrubs bank statements with 99%+ accuracy, and prepares files the moment they hit your inbox. Your team spends time underwriting deals, not typing data.

What Heron Delivers

- Instant bank statement scrubbing for deposits, returns, cash-flow patterns, and debt positions.

- Full KYB checks, SOS checks, and web presence analysis to confirm business legitimacy early in the workflow.

- Instant court research to surface legal red flags without slowing your day.

- Auto-detection of missing or bad files, keeping kickouts out of underwriting queues.

- Risk checks in the background (UBO, fraud patterns, cash-flow declines) while your team stays focused.

- Decision-ready data synced to your financial CRM, removing manual updates.

- Classification of 50+ document types, including ISO apps, tax forms, contracts, and financials.

- Underwriting support with clean spreads, summaries, and trends surfaced in seconds.

Heron gives you a steady loan workflow from intake to decision, removing the tasks that slow teams down and helping you close more deals with the same headcount.

FAQs About Loan Processing Workflow

What are the five C’s of loans?

The five C’s are Character, Capacity, Capital, Collateral, and Conditions. They help funders understand how stable a business is, how it manages money, and how likely it is to repay. MCA teams often focus on cash flow strength, existing positions, bank activity, and overall business behavior when reviewing these factors.

What are the six phases of the loan process?

The six phases are:

- Application – Collecting the file and first documents.

- Review – Checking basics, cash flow, and business details.

- Verification – Confirming identity, KYB information, and key numbers.

- Underwriting – Evaluating risk and deal structure.

- Approval & Terms – Issuing offers and confirming details.

- Funding – Final checks and sending the approved amount to the business.

These steps make up the core of most loan processing workflows.

What are the four steps to processing a loan?

The four steps are:

- Intake – Receive the file and gather documents.

- Review – Check cash flow, business details, and early risks.

- Decision – Underwriting reviews the file and sets terms.

- Funding – Confirm final documents and release funds.

Many MCA teams rely on tools like Heron to make these steps faster and cleaner.

Is a loan origination workflow the same as loan processing?

No. A loan origination workflow focuses on the first part of the loan journey, including intake, early review, and document checks. Loan processing includes origination but also adds cash-flow review, credit checks, underwriting, approval, and final funding. Origination is one part of the process, while full processing covers the entire path from application to funded deal.