Ever open your inbox and see five new business loan files waiting, each with different documents and follow-ups already piling up?

One bank statement leads to another request. A missing page turns into another email. And before long, the day feels heavier than it should.

This is the daily pace for MCA funders, brokers, and insurance teams reviewing businesses applying for capital. Manual steps inside a loan processing workflow slow reviews and pull attention away from real decisions.

Digital loan processing offers a steadier solution for handling that load. It supports the same workflow teams already follow, but replaces time-consuming paperwork and manual checks with digital support.

In the sections below, we’ll break down what digital loan processing really means and how it helps teams keep files moving without adding pressure.

TL;DR

- Digital loan processing helps MCA funders, brokers, and insurance teams move business loan files faster by reducing manual work early in the workflow.

- It supports the loan processing steps teams already follow by organizing documents, cleaning bank data, and surfacing issues before underwriting begins.

- With cleaner files and fewer follow-ups, underwriters spend more time reviewing deals and less time fixing paperwork.

- Tools like Heron prepare business applications upfront, helping teams handle higher volume without adding staff or changing how decisions are made.

What Digital Loan Processing Means for Lending Teams

Digital loan processing uses digital tools to streamline business loan applications and reduce manual effort.

Instead of relying on paper-based processes, teams handle applicant information, documents, and data in one place while following the same digital loan origination process they already know.

For financial institutions, credit unions, and traditional lenders handling commercial loans, this shift replaces repetitive tasks that slow reviews.

Automated systems pull data from a borrower’s bank account, organize paperwork, and reduce human error during underwriting and risk assessment.

Teams still make the credit decisions. The tools simply prepare the file.

As digital demands rise across the industry, digital loan processing helps small businesses access capital faster while teams manage risk, support regulatory requirements, and improve operational efficiency.

The result is clearer decision-making, faster approvals, and a more consistent lending experience, which are some of the key benefits noticeable at first.

How Digital Loan Processing Fits Into a Loan Processing Workflow

Digital loan processing supports the loan processing workflow your team already follows. It does not replace judgment or change how deals move.

It simply helps each step stay clean and consistent as businesses apply for capital.

Here’s how it fits across the workflow:

- Intake - Digital loan origination systems collect files from loans online and keep submissions organized from the start.

- Early review - Clean data sources improve transparency and help teams spot gaps before reviews slow down.

- Underwriting - Data analytics and light automation support risk management while underwriters stay in control.

- Funding - Tools like electronic signatures speed final steps and help reach faster loan approvals without cutting corners.

For traditional lenders and companies handling different loan types, this digital transformation supports a smoother flow, stronger loan performance, and improved customer experience.

It also helps ensure regulatory compliance through clearer records and better integration with existing services.

When Does Digital Loan Processing Make Sense for Busy Teams?

Digital loan processing matters most when volume rises, but the team stays the same.

This often shows up during busy funding periods, when MCA brokers send in multiple submissions at once or when insurance teams face tight turnaround expectations.

Files arrive in different formats, documents vary in quality, and small gaps start to slow everything down.

It also becomes clear when timelines shrink. Same-day offers, fast decisions, and quick follow-ups leave little room for manual cleanup. Every missing page or unclear bank statement adds friction that the team does not have time for.

In these moments, manual workflows begin to strain — reviews feel rushed, queues grow, and underwriters spend time fixing files instead of reviewing deals.

Digital loan processing helps teams stay steady during pressure points. It keeps files organized and review-ready, so work continues smoothly, even when submission volume or urgency increases.

What Changes Once Digital Loan Processing Is in Place

Most delays don’t come from underwriting decisions, but from the work around the file.

In traditional lending, teams lose time sorting documents, cleaning up bank statements, and chasing missing details from businesses applying for capital.

Digital loan processing reduces that friction early. Files arrive cleaner and easier to review, which cuts down on emails and follow-ups and adds convenience to the day.

Cash flow reviews move faster when bank data is clear, and early business checks surface issues before they reach underwriting.

As a result, underwriters spend more time reviewing deals and less time fixing files. Decisions feel steadier, even when volume rises. Teams can handle more submissions without adding pressure to the day.

The biggest change is not speed alone. It’s consistency. Work feels more controlled, reviews stay on track, and the lending process becomes easier to manage across busy days.

Heron: Built to Support Modern Loan Processing Workflows

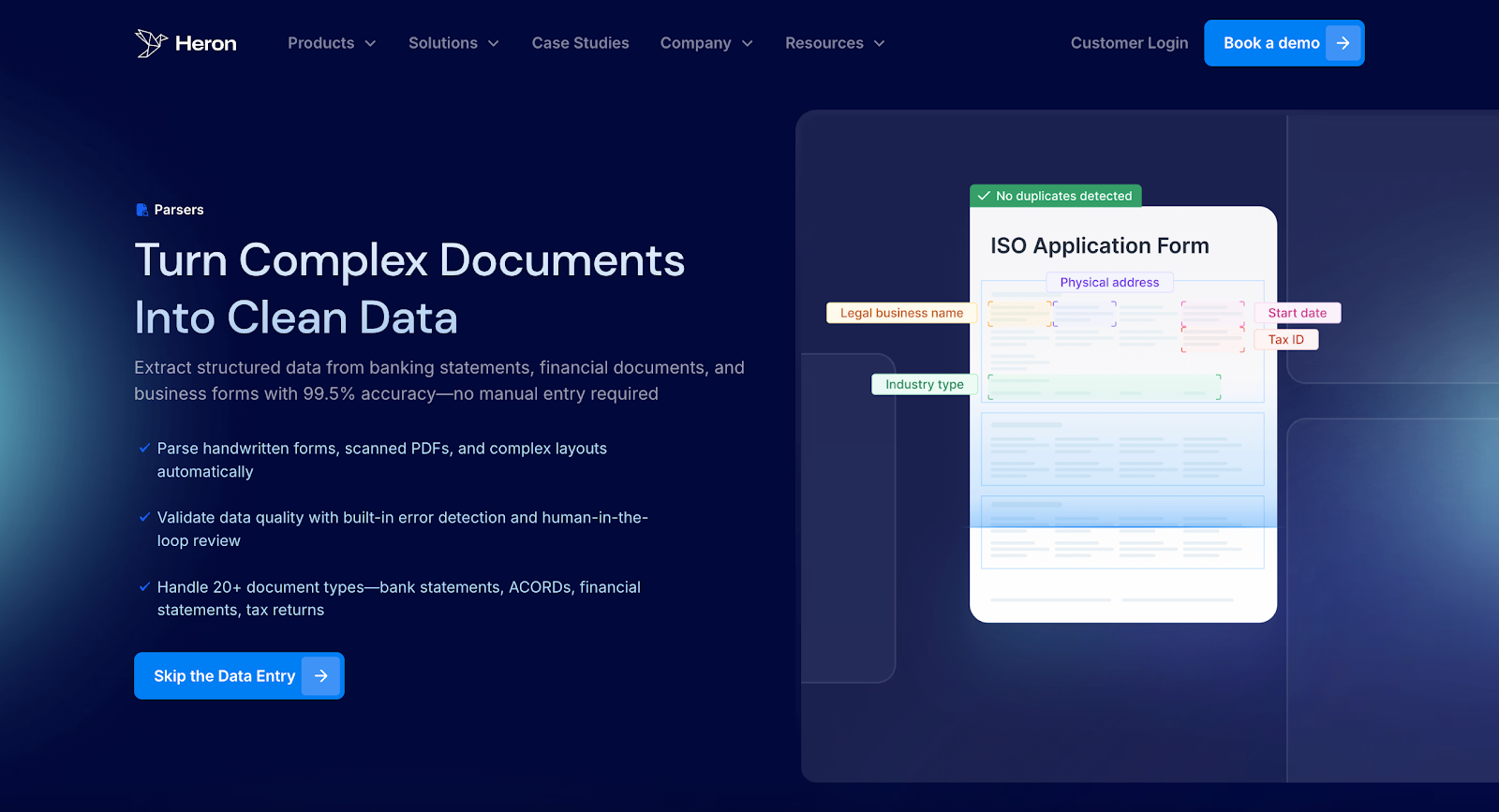

Heron supports digital loan processing by preparing files before they reach underwriting. It works inside the financial workflow MCA brokers, funders, and insurance teams already use.

When a business applies for a loan, Heron steps in early to clean up documents, surface risks, and organize data so teams are not stuck fixing files later.

More than 130 financial teams use Heron to handle high-volume submissions without adding headcount or slowing decisions.

Instead of spending 10-15 minutes per file on manual review, Heron scrubs and organizes data in seconds.

It plugs directly into your existing CRM or system of record, so there is no rebuild and no new process to learn. Your team stays focused on underwriting and closing deals, not paperwork.

What Heron does inside digital loan processing

- Bank statement scrubbing - Cleans deposits, withdrawals, balances, and trends so cash flow reviews start clear.

- KYB and SOS checks - Confirm that businesses applying for loans are real, active, and properly registered.

- Web presence analysis - Adds context around how a business operates online before underwriting begins.

- Instant court research - Surfaces legal red flags early, without slowing the review.

- Early risk signals - Flags missing files, fraud patterns, and cash flow concerns before they reach underwriters.

- CRM sync - Pushes decision-ready data directly into your financial CRM, removing manual updates.

Heron helps teams move business loan files faster without adding staff. Some companies have cut credit review time by 99%, turning a long manual step into a quick checkpoint.

FAQs About Digital Loan Processing

What is the digital lending process?

The digital lending process is how businesses apply for and move through loan reviews using digital tools instead of paper. Files come in online, data is organized automatically, and teams review cash flow, risk, and terms in one place. This setup helps MCA funders, brokers, and insurance teams move faster while keeping the same review standards.

How do digital loans work?

Digital loans work by collecting business applications, bank data, and supporting documents electronically. Systems use artificial intelligence and machine learning to organize information and flag gaps, but people still make the final decisions.

Can I get a digital loan with bad credit?

Digital loan processing does not change credit requirements. Many business funding decisions focus on cash flow, revenue, and risk signals rather than credit alone. Terms like approval and interest rates still depend on the funder’s criteria and the strength of the business.

What are the risks of digital lending?

The main risks come from poor data or missing checks. Strong digital loan processing reduces this risk through early research, clearer files, and reviews that stay accessible to the team. Human oversight remains critical at every stage.