Many teams ask the same question today: Will AI replace underwriters?

In short, no. The concern shows up more often because daily workloads keep rising. Files come in faster, formats vary, and the pressure to move deals forward never stops.

The insurance industry feels this shift the most, especially as expectations grow on both speed and accuracy.

So when people hear more about artificial intelligence and new underwriting workflows, the worry comes up. It’s not fear of the tech itself. It’s the weight of the work.

When the day already feels packed, any new tool can sound like it aims to replace people instead of helping them.

But AI sits in a different place than many expect. It supports the work underwriters do instead of taking it away. It clears the busy tasks so humans can stay focused on the parts that matter.

Let’s walk through what that balance looks like and why the underwriter’s role remains central in every decision.

TL;DR

- AI will not replace underwriters. It handles repetitive work so humans can focus on judgment, risk calls, and real conversations with brokers and merchants.

- Underwriters still manage context, nuance, exceptions, and final decisions that AI cannot make.

- AI speeds up reviews by scrubbing files, pulling key numbers, catching missing items, and preparing clean submissions.

- Leaders see smoother pipelines, more capacity, and fewer delays when manual prep disappears.

- Tools like Heron use AI to automate intake, scrubbing, fraud checks, and verification so underwriters stay focused on decisions instead of admin tasks.

Why People Think AI Will Replace Underwriters

This question keeps spreading because the conversation around technology keeps shifting.

New AI tools appear every month, and many teams hear bold claims about faster reviews, fewer mistakes, and automated steps inside the insurance underwriting process.

With so much noise, it becomes hard to tell which tools support underwriters and which tools claim to replace them.

At the same time, companies talk about efficiency, cost pressure, and technology upgrades. That creates tension. Underwriters wonder how far automation will go and where their work fits as systems take on more data tasks.

But the concern doesn’t come from AI’s ability to judge risk. It comes from the way these conversations get framed.

When people hear “automation,” they sometimes hear “replacement,” even when the goal is simply to remove repetitive steps that slow down reviews, not remove the underwriter.

The question exists because the space is shifting, not because teams want machines making decisions.

What Underwriters Do That AI Cannot Replace

Even with new AI models and stronger underwriting automation, some parts of the job stay firmly human.

Underwriters handle work that needs human judgment, real-world context, and direct conversations. AI systems help with routine steps, but they cannot replace human underwriters in areas that shape outcomes.

Here’s what still needs people:

- Context and nuance - Underwriters look beyond numbers. They spot patterns, tone, intent, and small details that shape real risk analysis. Machines can analyze data, but they miss the “why” behind it.

- Risk sense - Years of experience guide decisions. This guides how teams read risk factors across files, industries, and unusual cases.

- Exceptions - Complex cases need human oversight because rules don’t cover every situation. Some files need flexibility instead of strict automation or tools to automate risk assessment.

- Conversations and relationships - Brokers, merchants, and clients rely on the human touch, especially when they need clarity or pushback.

- Ethics and responsibility - Only people take responsibility for final calls. Humans weigh fairness, intent, and impact in ways tech cannot.

Where AI Helps Underwriters Move Faster in the Insurance Underwriting Process

The slowest parts of the day often come from work that doesn’t need judgment. This includes manual data entry, digging through mixed files, and sorting details that pull attention away from actual review work.

AI helps clear most of that load so underwriters can focus on decisions instead of routine tasks.

Here’s where AI makes the biggest difference:

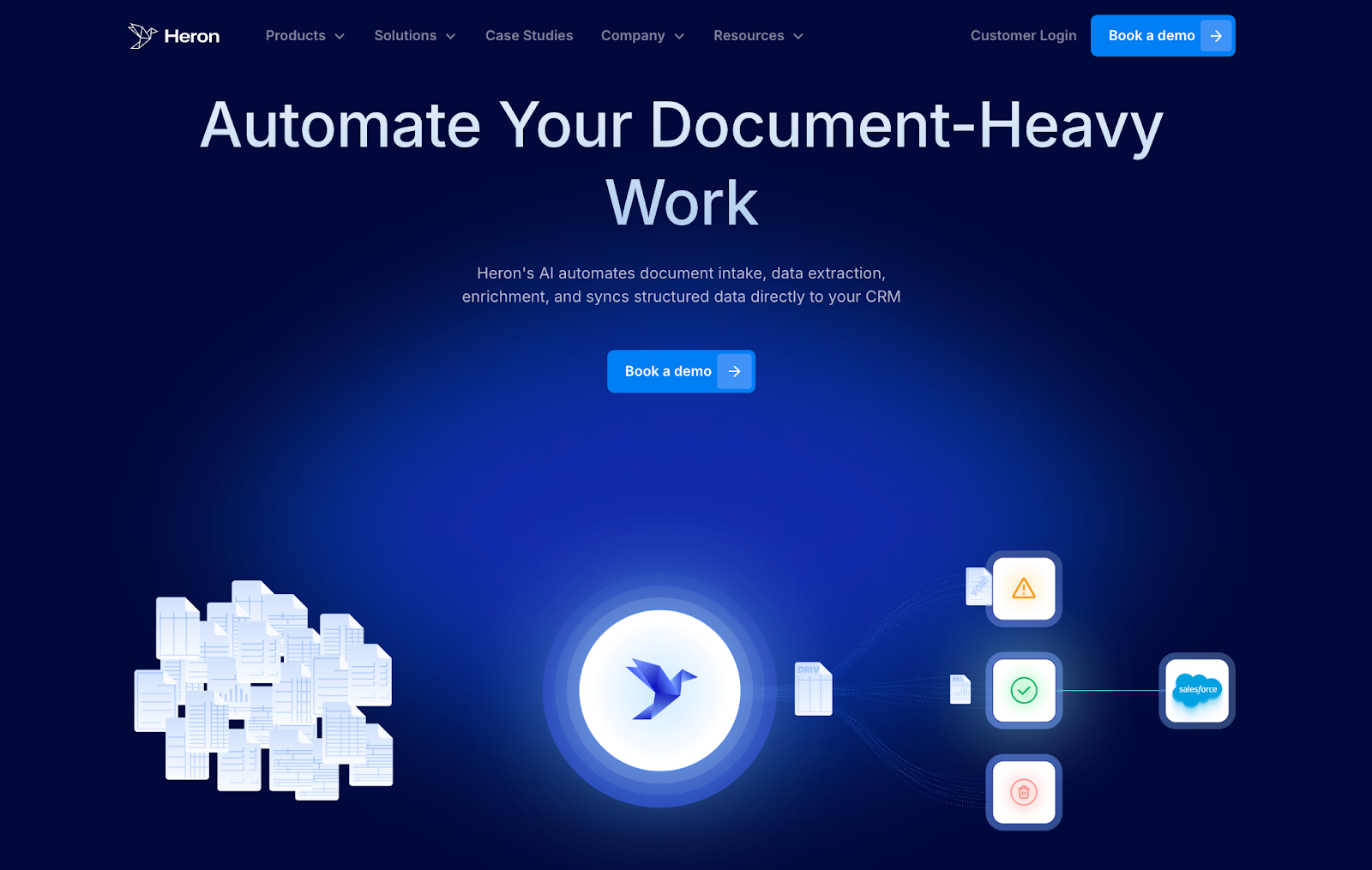

- Collects data - AI pulls information from PDFs, ISO apps, and statements.

- Reads messy files - Modern machine learning reads formats that would normally take minutes or hours to clean.

- Pulls out the numbers that matter - It organizes deposits, returns, balances, and other fields into simple views.

- Flags missing items early - Missing documents, gaps, or unclear values get caught before review.

- Keeps information clean and easy to check - AI gives underwriters clear layouts and actionable insights that improve underwriting efficiency.

These steps support the underwriter. They do not replace the judgment needed to manage risk or guide final decisions.

Why AI + Underwriters Create Stronger Decisions

When AI takes on the background work, underwriters gain more space for real judgment. Instead of repeating tasks listed earlier, this section now focuses on decision quality, risk consistency, and long-term outcomes.

Underwriters can apply their deep understanding of risk to each file without rushing through critical checks. This balance strengthens decisions across an insurance company because teams approach risk the same way, even when volumes rise.

AI also supports cleaner outcomes. When information is prepared and organized, the chance of human error falls, and risk calls become clearer.

This makes it easier for teams to revisit past decisions, explain reasoning to auditors, and stay aligned with a shifting regulatory landscape.

Modern tools, including those powered by large language models, surface the right data without replacing the human intervention needed in complex or sensitive situations.

Underwriters still decide on coverage, push back when something feels wrong, and guide outcomes for merchants and customers.

AI speeds up the work. Underwriters keep the quality steady.

How Leaders Feel the Impact Day to Day

When AI takes on the repetitive parts of the workflow, the improvement shows up in places managers track every day.

Instead of the team getting stuck on prep work, leaders see smoother pipelines, steadier pacing, and fewer surprises during the week.

Deals move from intake to review without unnecessary stalls, and the team avoids the slowdowns that come from digging through files or waiting on missing details.

Capacity also opens up. Managers can take on more submissions without expanding the team, and training becomes easier because new underwriters step into cleaner, more organized workflows.

This keeps service levels stable even during busy cycles, which helps both brokers and every partner waiting on decisions.

With repetitive work handled upfront, leaders get a clearer view of workloads, better predictability across the queue, and stronger consistency from one underwriter to the next.

The team gains efficiency without losing the human element that guides real decisions.

Work Smarter With Heron Supporting Your Underwriting Team

Underwriters move faster when the front end of the workflow is clean, structured, and ready for review.

That’s exactly where Heron makes the biggest impact. Instead of spending 10–15 minutes scrubbing each file or digging through messy emails, underwriters get decision-ready data within seconds.

Some MCA funders now handle up to 6–7x more submissions with the same team, based on real results from Heron case studies.

Heron plugs directly into your existing system, including Salesforce, LendSaaS, Zoho, Cloudsquare, Origami, Novidea, and more, so your team doesn’t change how they work.

You forward the submission, and Heron returns clean data, fraud checks, eligibility signals, and missing-item flags instantly.

Heron keeps underwriters focused on decisions, while operations stop triaging inboxes, brokers get answers faster, and funders move deals before competitors even open the file.

Key features that matter to underwriting teams:

- Bank statement scrubbing in seconds with revenue, NSFs, debt positions, and fraud signals.

- Submission intake automation for sorting, naming, and routing documents from the inbox to the financial CRM.

- KYB checks, SOS checks, and web presence analysis for quick entity verification.

- Instant fraud detection for manipulated statements and mismatched uploads.

- Kick-out and appetite checks so underwriters only see qualified files.

- Automated decision intake for brokers handling 500–1500 daily funder responses.

- Structured data syncing straight into your CRM. No uploads, no spreadsheets.

Heron gives teams speed, accuracy, and scale without hiring more staff. A direct lift in underwriting capacity and a clearer path to funding more deals.

FAQs About AI Replacing Underwriters

What is the future of underwriting?

Underwriting will rely more on AI to handle repetitive administrative tasks, but human judgment remains essential. As submissions grow and insurers assess more complex risks, underwriters guide the final decisions and interpret details that AI cannot fully understand. The role becomes more technical and more strategic, not less important, over the next five years.

Is underwriting a dying field?

No. Underwriting is evolving, not disappearing. AI helps process vast amounts of data faster, but underwriters still evaluate context, intent, and the details that shape real outcomes for insurance policies and funding decisions. The field continues to grow because businesses rely on skilled people who can weigh risk with real expertise.

Which jobs cannot be replaced with AI?

Roles that require reasoning, negotiation, and nuance, including underwriting, claims review, and commercial property evaluation, cannot be fully automated. These jobs depend on conversations, judgment, and understanding how decisions lead to real financial outcomes for a business.

Will AI replace mortgage lenders?

AI can automate paperwork and speed up pre-qualification, but it cannot replace the full role. Mortgage specialists, funders, and similar roles require guidance, explanation, and trust, especially when borrowers make long-term commitments. Humans remain central in lending decisions because people want clear advice, not an algorithm making the call.